I edit more and write less these days, but even when I do write I often forget to link to it here. I’ll try to be better in 2021.

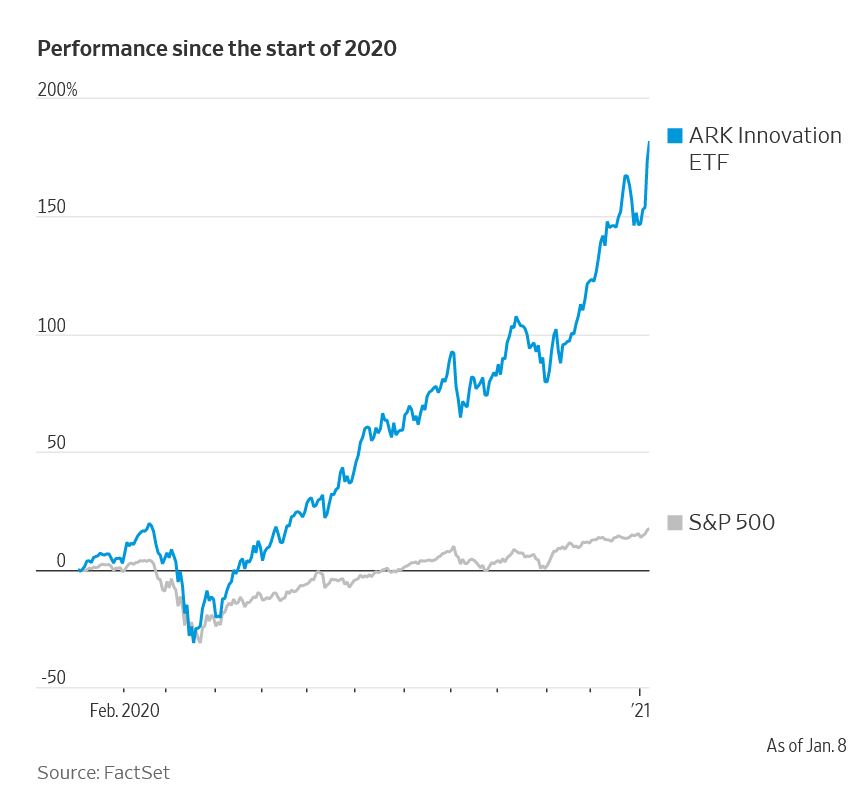

One thing I wrote recently generated an unusual amount of reader email, split about 40-60 between congratulatory and outraged. I said that star fund managers are to be avoided and I used the example of Cathie Wood, whose main exchange traded fund at ARK Invest grew assets by 1,000% last year and gained nearly 160%. She bet big and won on hot stocks like Tesla and biotechs that benefitted from Covid-19 speculation.

I am apparently a misogynist or don’t understand her genius or both. Anyway, the evidence is pretty strong that jumping on the bandwagon once a fund manager graces magazine covers isn’t a great idea whether that manager has a “Y” chromosome or not. You can read more about managers like Ken Heebner and Bill Miller in my book.

The column starts out with a “famous last words” puff piece from The Motley Fool titles “Move Over, Warren Buffett : This Is the Star Investor You Should Be Following.”

So read the headline on a year-end article from retail investing advice site Motley Fool touting the performance of fund manager Cathie Wood. Variations on the “Buffett is done” theme have been around since at least the tech bubble, while the cult of star mutual-fund managers goes back to the 1960s. Such commentators have eventually eaten their words.

Ms. Wood is a savvy businesswoman, but is she a savvy investor? Stock picking skill is very rare and even harder to discern when the manager is riding a hot category. In a bull market propelled by dumb retail money, everyone is a genius. It takes many years to establish whether success is random. And, as I point out, star manager’s performance is often worse than random on the downside. The most promising active funds are those that lagged their peers recently or got a low rating from a firm like Morningstar.

Fund managers are often compared with dart-throwing monkeys. That might be too flattering for those who get the most attention. Hot funds’ performance is often worse than random on the downside. A regularly updated study on the persistence of investor performance from S&P Dow Jones Indices shows that just 0.18% of domestic equity funds in the top quartile of performance in 2015 maintained that through each of the next four years—less than half what one would have expected by pure chance. And of course most actively managed funds lag behind the index to which they are benchmarked because of fees and taxes.

Anyway, the tone of the emails has made me more convinced that some investors in “disruptive innovators” have lost touch with reality. Congrats if you were early — the fund’s performance is pretty impressive (see chart below) — and be careful if you were late.

Leave a comment