“Mr. Bond, they have a saying in Chicago: ‘Once is happenstance. Twice is coincidence. The third time it’s enemy action.’” – Auric Goldfinger

…

Last October about 3.5% or $2.4 trillion was wiped off of the U.S. stock market’s value in one afternoon. As is often the case, bitcoin was no safe haven—it fell more than twice as much.

The spark for the selloff: President Trump posted on his Truth Social account that the U.S. was considering fresh trade measures against China. Two anonymous accounts on a crypto exchange placed big bets that bitcoin’s price would drop, with the last trade being made one minute before the post. They earned about $160 million.

Months earlier there had been an even wilder swing during trading hours when Trump announced a pause on his “Liberation Day” tariffs. The Dow jumped by 2,963 points, its largest intraday gain on record. Minutes earlier there had been a flurry of activity in call options on various exchange traded stock funds.

Those derivatives would have expired worthless within three hours had there been no substantial market move. Instead, whoever bought made a profit of, according to one estimate, 1,200%.

Were they half lucky or too lucky by half? Judge for yourself: Here’s a gift link to a thorough writeup by one of my colleagues that goes through all the episodes so far.

If your image of this nation’s securities regulators was formed by Bud Fox being led away on the trading floor in handcuffs in “Wall Street,” here’s an update. We’ve gone from having financial Keystone Cops to basically having no sheriff in town.

Insider trading isn’t a victimless crime, but it’s an abstract one since it picks millions of honest savers’ pockets all at once. The practice is far more damaging when we get the impression it’s being done with impunity by well-connected people. That’s how the U.S. stock market was for much of its history and why the public mostly stayed away, keeping their savings in the bank or under the mattress instead.

That’s bad for prices because investors will demand a higher return for the possibility of being swindled. As damaging as a loss of public trust would be to our nest eggs, though, there’s a more immediate danger now—a threat to our physical safety.

Earlier this month, just before Trump announced that the U.S. was having “productive conversations” with Iran and would delay attacks on its infrastructure, someone made a gigantic bet that oil prices would fall. Brent crude futures fell from more than $112 to less than $100 seconds after that post.

Buying futures can magnify a bet tenfold or more. Those well-timed trades for hundreds of millions of dollars made someone very, very rich.

That particular episode didn’t threaten our servicemen. Some earlier ones might have.

Just as U.S. forces began striking Iran, big bets were made on Polymarket that the attack would begin that day. Analytics firm Bubblemaps found evidence that the same anonymous accounts had made successful wagers on the strike last year on Iran’s nuclear facilities. And in January a series of bets were made that Venezuelan strongman Nicolás Maduro would lose power, with the final one less than an hour before Trump ordered him removed.

A huge stock or commodities market transaction right before a military decision is a “tell” to a country’s adversaries, but at least it doesn’t give much warning. It also leaves a paper trail if anyone bothers following it.

Prediction markets make it much easier to remain anonymous and to make a highly specific bet. Right now on Polymarket you can place a wager about the Iranian regime collapsing by the end of April (a 7% implied chance), a U.S.-Iran ceasefire by the end of June (59%), or China invading Taiwan this year (10%). There are also all sorts of specific contracts tied to a certain day for wagers on Iranian or Hezbollah missiles hitting Israel (nearly 100% most days).

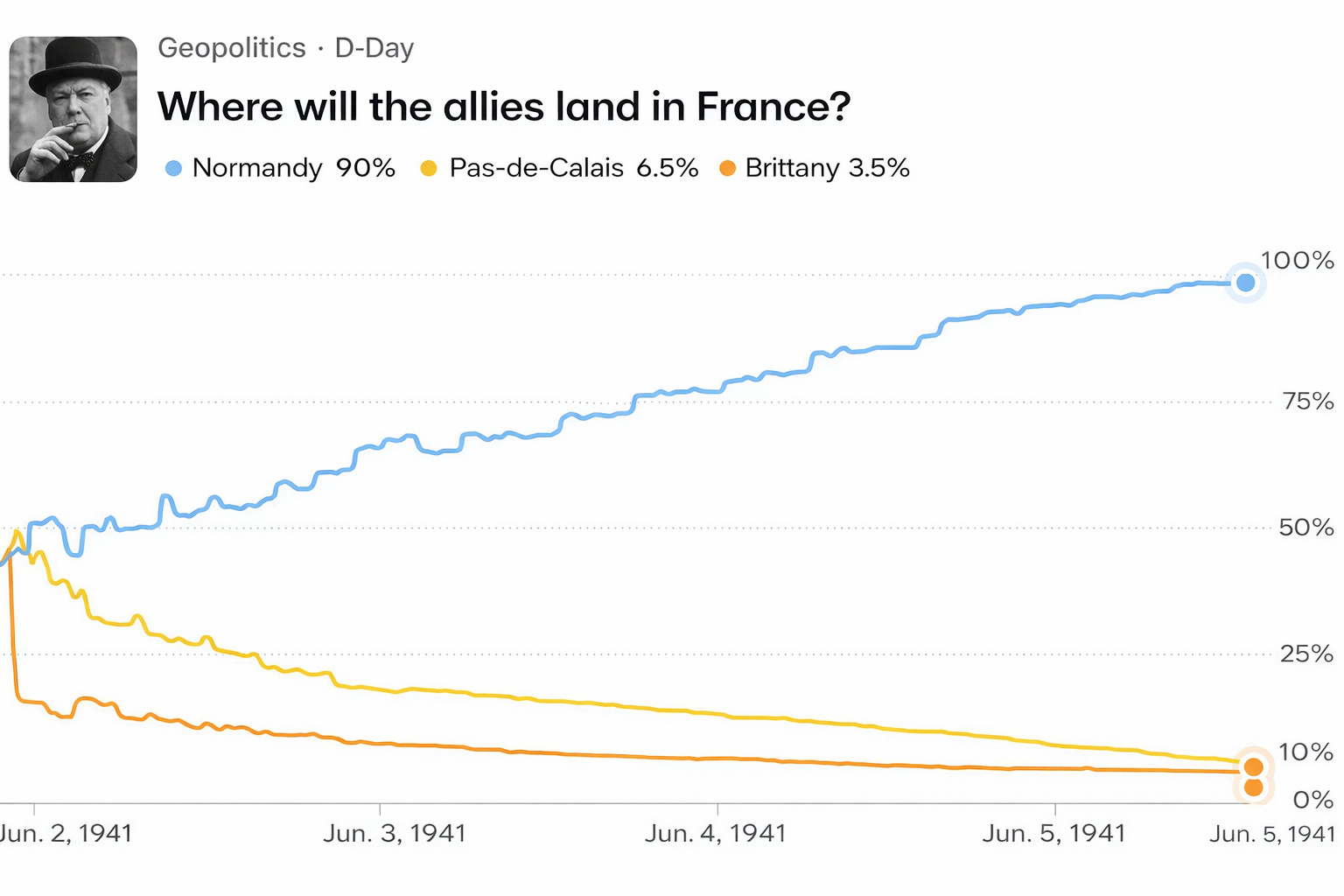

It isn’t just macabre—it’s dangerous. Imagine being allowed to put money on such things during some pivotal event in history like D-Day. An entire U.S. army group with a fake staff, radio traffic, and inflatable tanks was created to give the Germans the strong impression that the attack would hit Pas-de-Calais in July 1944, not Normandy in June.

In a country as densely-populated as Great Britain, and with at least hundreds of people involved in the deception, it would have been easy to make what seemed like a harmless few quid on what you knew. But even small bets on something so specific can move a market.

Any German agent with half a brain would have alerted Berlin. The plot of Ken Follett’s “Eye of the Needle” is about a master spy discovering the phony army but insisting on delivering the news himself rather than by radio.

As we know, the deception was successful. Even after the landing at Normandy, German forces were held back for what seemed like a more-likely actual invasion site farther north. Had the D-Day landings been a failure, historians estimate hundreds of thousands or even millions more deaths. Much more of Europe would have wound up living behind the Iron Curtain for decades.

I’m not a big fan of gambling, but it’s hard to stop, even where it’s technically illegal. But this is different, and allowing wagers to be made through anonymous accounts is especially dangerous. Any normal person should be upset that people seem to be profiting off of access to market moving announcements. They should be outraged that they’re profiting right before our military undertakes dangerous missions.

It really shouldn’t matter if the bettor’s brother-in-law works on an aircraft carrier or if they’re related to a high government official. However embarrassing the findings are, anyone doing this needs to be investigated and punished in the most public and harsh way as a deterrent. And these contracts should be illegal, period.

There are plenty of things to gamble on without passing on secrets to our enemies.