Remember the DC-10? I’m dating myself by telling you that I recall flying on the widebody jet when I was about nine years old. I couldn’t have been much older than that because all of the ones operating in the U.S. were grounded for a while in June 1979. This came after the deadliest airline crash in U.S. history not related to terrorism, American Airlines Flight 191, which killed 273 people. A much longer grounding, more than a year-and-a-half, resulted from the deaths of 346 people in two crashes of the Boeing 737 MAX. And all U.S. air traffic was shut down for days after the 9/11 terror attacks almost 20 years ago which resulted in almost 3,000 fatalities.

While I’m not arguing that any of these were overreactions, they are a sign of how bad we are at weighing danger. I remember many people saying that, even once cleared to fly, they wouldn’t get on a DC-10 or a 737 MAX. Many skipped flying altogether for months after 9/11. Yet there seems to be virtually no concern today about a threat that killed 1,275 Americans in just the past two days – the Covid-19 pandemic.

Proms are going on unmasked, basketball arenas are full of fans with a few people wearing them draped around their chins, and airplanes are packed. Thank goodness 50% of American adults have now been fully vaccinated, but that leaves half who haven’t been. The people who are most likely to eat in a crowded indoor eatery or other high risk activities are also less-likely to be among the half concerned enough about catching or passing on the coronavirus to ever get a vaccine.

I’m not advocating for a lockdown, but the lack of caution is interesting. Somehow two or three hundred deaths from an air disaster gets us spooked, a few thousand dead from a domestic terror incident has us terrified, but 600 deaths a day with many more hospitalized are an acceptable risk.

Why do we think this way? Is it that a deadly fireball on the evening news seems scarier than the abstract thought of hundreds of people spread all over the country who are probably strangers gasping for breath and dying alone of a respiratory illness? An alternate explanation is that 600 is a whole lot better than the 3,000 plus a day who were dying back in January and that we’ve put the danger in perspective.

The second explanation might be convincing if it weren’t for the fact that lots of people weren’t being at all careful then either. My family and I drove from New Jersey to Florida for our one and only trip of the pandemic over New Year’s. As soon as we got south of the DC suburbs the level of caution began to evaporate. Pee breaks were filled with anxiety as we walked into rural convenience stores and motel lobbies where patrons and employees seemed blithely unaware of the global pandemic.

But then maybe we were the ones who misunderstood risk. In terms of fatalities per mile traveled, a road trip in non-Covid times is about 750 times as likely to be fatal per mile as a plane journey. Being locked in a pressurized metal tube with a hundred or so mostly-masked strangers for a few hours each way might not have been too much more likely to result in infection than those bathroom breaks.

All’s well that ends well as we didn’t get sick or crash, but maybe we would have been safer flying — even in a DC-10.

The hottest thing in investing these days is using ESG criteria (environmental, social, and governance). Count me a skeptic. Yes, I have seen studies showing that, for some specific period, such funds have outperformed the market. They usually are funds that have avoided fossil fuels during a particularly bad stretch for energy companies or are loaded up with tech stocks during a really good period.

Should you be forced to invest in a company that conflicts with your ethics? No, I guess not, but then investing in a fund isn’t the same as giving a company money. On the other hand, if you really want to put your money where your mouth (and wallet) is, why not make as much money as possible and then give it to a cause of your choice?

Let’s say that ethically and religiously focused funds, which reduce the number of possible companies in which you can invest, will do just as well over time as a fund that owns the whole stock market. The fees they charge you for doing that will still eat into your return, which is why ESG is a brilliant marketing concept but not such a smart way to invest.

But you know what really isn’t smart? I read today in the Wall Street Journal that Trump allies are now getting into the fund management business to promote “Unwoke” funds.Pictured up top is Kevin Hassett, the co-author of Dow 36,000. Just a reminder that this book came out almost 22 years ago and the Dow hasn’t hit that milestone yet, so caveat emptor. Below is the description of the criteria behind their “Society Defended ETF.”

With respect to the 2nd Amendment Score, the base score will increase for monetary donations that support the right to bear arms or decrease for monetary donations that support gun control laws based on the dollar amount. The degree to which companies provide direct or indirect support to organizations which support gun free zones, support of gun control legislation, oppose stand-your-ground-laws, oppose concealed carry, support banning of firearms or refusal to do business with the firearms industry, and related advocacy groups or legislation will lower their 2nd Amendment Score.

Let’s just leave the gun control debate out of this and look at dollars and cents. If the companies, which I guess you could call anti-ESG, also do just as well as the market then you are paying unnecessary expenses to own the libs. At 0.75%, this fund charges you 0.7 percentage points more than a very low cost index fund. If the market goes up by 8% a year for the next 40 years then a $10,000 investment today would be worth nearly $50,000 less than in a plain vanilla fund. So if you love guns, or whales, or hate coal, or whatever, my recommendation is to just make the best investment possible and then get a nice tax-deduction at the end for contributing part of your windfall.

If you were to hold a contest to design the most-enticing name for a company right now you couldn’t do much better than “RocketFuel Blockchain.” And if you were to pick a bank to associate with it now or really any other time than Goldman Sachs would top your list. But read the fine print before you buy shares in a company by that name written up by Goldman … a lot of people seem not to have bothered.

“Following the release on April 1 of a news release titled “Goldman Small Cap Research Publishes New Research Report on RocketFuel Blockchain, Inc.,” the penny stock surged by as much as 335% in four days. Several lines down is a notice that the research firm, which accepts payment for reports, “is not in any way affiliated with Goldman Sachs & Co.”

And the report’s subject, formerly known as B4MC Gold Mines Inc., and before that as Heavenly Hot Dogs Inc., doesn’t appear to have any revenue and maybe not even a product, based on litigation about a patent that expired. The report was written by an analyst who, while he appears not to have lit the world on fire at more-established firms, has an auspicious name: Rob Goldman.”

The documentary category is the first one that comes up when I scroll through Netflix. One of the top choices it offered me was “The Last Blockbuster” which is, as you might have guessed, about the very last Blockbuster Video store in the world (there was one in Perth, Australia that closed in 2019). The chain went bankrupt in 2010 and is sort of a punchline these days, but it’s nice to see at least one hanging on for now. I wrote a short Overheard about it on Friday.

The ironic thing is that it was Netflix that basically put Blockbuster out of business and is now profiting from a film about the very last one. Back in 2000 Blockbuster made what is one of the greatest business blunders in history by turning down an offer to buy Netflix for $50 million. It is worth almost 5,000 times that much today.

According toThe Oregonian, the documentary’s popularity has revived the store’s fortunes with people buying lots of Blockbuster swag. If they’re one of the few people on the planet without a Netflix account, they can even rent a DVD copy of “The Last Blockbuster” there.

One of the more overused clichés is “it’s like turning around a supertanker.” As a landlubber, I’ll go ahead and assume that’s true in the literal sense. Financially-speaking, though, the business of hauling oil across the world certainly turned on a dime in the past year. Daily earnings collapsed by 99% from last March to the past week as carriers capable of holding two million barrels became very expensive floating storage tanks when there was a glut and are suddenly hunting for cargoes as big exporters try to buoy prices.

Jinjoo Lee and I wrote about the dramatic turn. Our takeaway was that things are looking up for this extremely cyclical business.

A year after their incredible good fortune, an equal basket of four energy shipping firms has lagged the S&P 500 by 70 percentage points over the past year and is right back to its long-term average ratio of price to book value. With life and energy demand returning to normal, this is no time for investors to walk the plank.

Some very interesting characters who advocate building homes on the world’s oceans tried to make lemonade out of lemons, but it went pear-shaped. They picked up a cruise ship cheaply since the industry is still idled by the Covid-19 pandemic and began auctioning cabins off to cryptocurrency enthusiasts — in dollars of course — to use as a floating base off the coast of Panama. The group rechristened the former Pacific Dawn the MS Satoshi.

Always do your research before an impulse purchase! As I wrote in a brief “Overheard,” the normal maritime laws still applied, even in a country known for its flags of convenience. The insurance requirements proved ruinous.

“Unfortunately, we will not be able to proceed because of archaic big insurance companies that cannot adapt to innovative new ideas,” wrote Ocean Builders Chief Executive Grant Romundt in an email to investors.

According to a Facebook fan page, MS Satoshi was sold for scrap and was last reported to be steaming to a yard in India to be broken up.

I edit more and write less these days, but even when I do write I often forget to link to it here. I’ll try to be better in 2021.

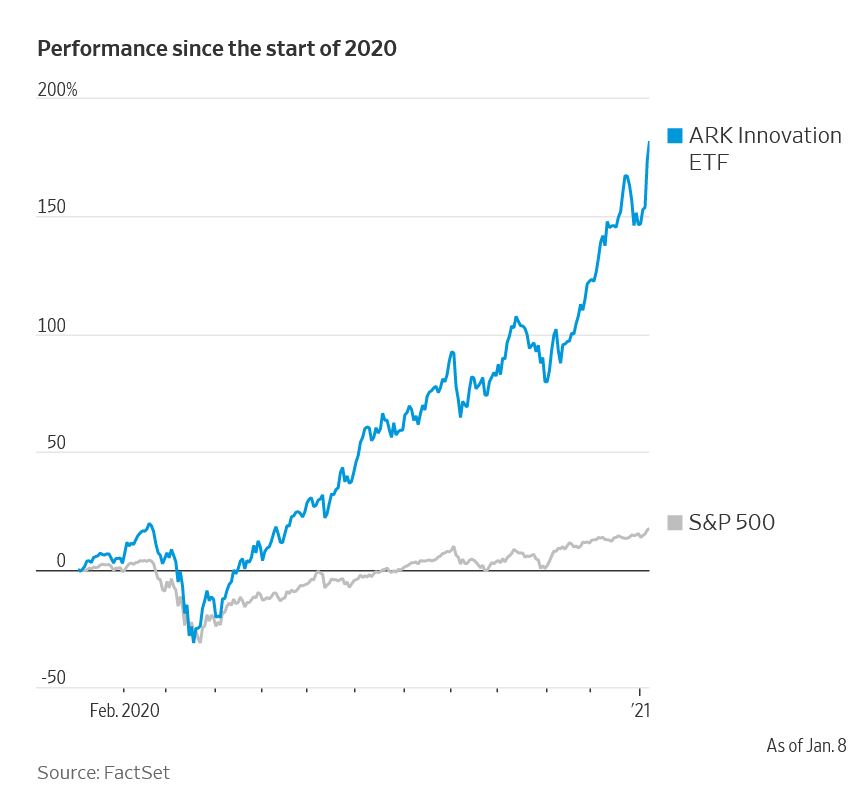

One thing I wrote recently generated an unusual amount of reader email, split about 40-60 between congratulatory and outraged. I said that star fund managers are to be avoided and I used the example of Cathie Wood, whose main exchange traded fund at ARK Invest grew assets by 1,000% last year and gained nearly 160%. She bet big and won on hot stocks like Tesla and biotechs that benefitted from Covid-19 speculation.

I am apparently a misogynist or don’t understand her genius or both. Anyway, the evidence is pretty strong that jumping on the bandwagon once a fund manager graces magazine covers isn’t a great idea whether that manager has a “Y” chromosome or not. You can read more about managers like Ken Heebner and Bill Miller in my book.

The column starts out with a “famous last words” puff piece from The Motley Fool titles “Move Over, Warren Buffett : This Is the Star Investor You Should Be Following.”

So read the headline on a year-end article from retail investing advice site Motley Fool touting the performance of fund manager Cathie Wood. Variations on the “Buffett is done” theme have been around since at least the tech bubble, while the cult of star mutual-fund managers goes back to the 1960s. Such commentators have eventually eaten their words.

Ms. Wood is a savvy businesswoman, but is she a savvy investor? Stock picking skill is very rare and even harder to discern when the manager is riding a hot category. In a bull market propelled by dumb retail money, everyone is a genius. It takes many years to establish whether success is random. And, as I point out, star manager’s performance is often worse than random on the downside. The most promising active funds are those that lagged their peers recently or got a low rating from a firm like Morningstar.

Fund managers are often compared with dart-throwing monkeys. That might be too flattering for those who get the most attention. Hot funds’ performance is often worse than random on the downside. A regularly updated study on the persistence of investor performance from S&P Dow Jones Indices shows that just 0.18% of domestic equity funds in the top quartile of performance in 2015 maintained that through each of the next four years—less than half what one would have expected by pure chance. And of course most actively managed funds lag behind the index to which they are benchmarked because of fees and taxes.

Anyway, the tone of the emails has made me more convinced that some investors in “disruptive innovators” have lost touch with reality. Congrats if you were early — the fund’s performance is pretty impressive (see chart below) — and be careful if you were late.

The origin of the phrase “hope is not a strategy” is disputed, but I generally hear it in a business context. I get the feeling that educators are going to become acquainted with it pretty soon.

By this time in August, schools in much of the country are scheduled to be filled with teachers and students. Many universities will start a week or so later. Some will teach remotely, but most are still slated to be in-person or some hybrid thereof. As the dad of kids in both high school and college and the husband of a school employee, I’ve been privy to the plans — if you can call them that — of the superintendents and provosts.

There was a peculiar kind of cognitive dissonance on display early in the Covid-19 pandemic by educators. Of all people, they’ve failed to learn. Back then I contacted the local superintendent and the college provost as cases were spreading about when they planned to send kids and teachers home. The answers were “it’s still rare here” when there was almost no way to get tested and when epidemiologists were warning that it was spreading exponentially.

That fear of looking dumb or alarmist repeated across thousands of districts and campuses probably cost thousands of lives. It’s somewhat excusable because it was hard back in February or early March to imagine what the world would look like just weeks later.

But what about now? Decision-makers all certainly know the meaning of “exponential” if they didn’t before. The U.S. has had 145,000 confirmed Covid cases in just the past two days and almost certainly many more unreported ones as people face long waits to get tested in the Sun Belt. What is more, a higher share of those cases is from a young, working-age cohort. Some schools in Florida, which reported over 15,000 cases on Sunday, open in as little as 20 days. I’ve been following private forecasts by Qijun Hong, a postdoc at Brown University, who has been producing remarkably accurate infection models for several weeks. Here’s his latest for Florida.

This is for confirmed cases. Of those tested, very few are children, but this week we learned that an incredible 31% of children tested randomly in Florida were positive. Even if the number of new cases in Florida in August is just half as high as Mr. Hong is projecting, is that low enough to reopen schools? The answer is almost certainly “no,” and here’s why.

In the first month of school alone, about 1 in 60 Floridian adults would be diagnosed with Covid-19. A school with 500 kids will easily have 40 teachers, aides, principals, coaches, secretaries and janitors plus a handful more substitute teachers — all part of that potential pool. And then there are easily 1,000 more adults who live with or regularly see those children who also could be diagnosed. And don’t forget the spouses of those teachers, janitors, principals, and substitutes — one of them could be diagnosed. Even if we assume that kids can’t spread the illness, the chances that at least one of those 1,100 adults doesn’t face quarantine or receive a diagnosis is tiny.

And if an asymptomatic teacher’s test is positive? With tests taking five or more days to come back, that employee will have had time to infect plenty of other adults and children. Will they all have to quarantine? And if they don’t, who wants to be the substitute teacher for the one who is positive? How many substitute teachers earn enough to take that risk and how many can the school system afford to pay? How sure are they that children can’t pass it on and at what age does it become more likely that they will? Try asking this question and getting a straight answer.

If the substitute starts feeling ill, will the system pay for his or her Covid tests or treatment even though they aren’t on the insurance plan? That substitute may have visited multiple schools, so which school is on the hook and will the teachers or students he or she met at each school then have to quarantine?

What if the first person diagnosed works in a middle school or high school? Well then he or she isn’t in contact with 25 kids daily but more like 125. In the case of a cafeteria worker it would be hundreds. What then?

The schools tell us they are taking steps, including lots of extra cleaning and social distancing, but how effective will they be? Having half as many kids in a room at a time will help, and so will mandatory masks, but kids aren’t especially careful or sensible. Even 100% compliance with mask-wearing and hand washing only would reduce, not eliminate, contagion. We know that an infected person spending an hour at a party or bar can infect several people. Even if schools are half day, the period of exposure will be longer.

The odds of any given school not being touched by Covid-19 are a bit better in most other states, but not great. One-in-100 or even one-in-500 adults infected in a month still makes an infection at a given school quite likely. With perhaps a third of teachers in higher-risk categories because of age or medical history, it is unfortunately only a matter of time before some of them are on ventilators.

The situation could be even worse for colleges hosting young adults who are most certainly capable of passing on the illness and who generally lack a healthy appreciation of their own mortality. What happens when a student in a dorm of 150 tests positive? He or she will have been contagious for a while. Remember when a single sick person who left the Diamond Princess sparked a lockdown of everyone else in their cabins? Weeks later 691 people on board had it. That was with passengers confined to their rooms and being brought their meals. Will colleges deliver meals to the student? Whose job will that be? And what about shared toilet and shower facilities? How many positive tests in a building before everyone is sent home? Is a dorm being set aside only for those who test positive or will they just be sent home to infect their parents and siblings? And what about international students who can’t go home? Will airlines or Amtrak transport infected students anyway?

I understand why colleges are so eager to have students return in person: money. Empty dorms and students deferring will put even more financial strain on them. I also understand why primary and secondary schools are doing it: pressure from politicians and from parents worried about their children falling behind or about who will watch them while they work. Unfortunately, the plans to keep everyone healthy are vague and ad hoc and we still know too little about this disease.

Instead of hazy, expensive, and unworkable plans, how about doing some serious planning for a better remote learning experience in the fall while the world waits for a vaccine? Online learning in the spring was subpar, but it doesn’t have to be.

It sounds a bit flippant at a time when so many people are seeing their nest eggs melt down on paper, but the message is important. Retail investors lag the market significantly because of timing errors and the biggest mistakes are made at junctures like these. If the 20% bounce from the coronavirus-fueled low turns out to be a dead cat bounce then it will stoke further pessimism and cause people to either sell or to have less of their wealth in risky assets such as stocks once the eventual turn comes.

I’d love to tell you when that turn will be, but I can’t and neither can anyone else. The important thing to remember, though, is that if you were comfortable having, say, 70% of your nest egg in stocks when the Dow was knocking on the door of 30,000 then you should feel the same way at 20,000 or (gulp) 15,000. The richest gains of the next bull market (no, I don’t think this recent bounce was the start of one) probably will come early on. They always have before.

For example, if you put $100,000 into a plain vanilla U.S. index fund at the very start of the last bull market in March 2009 and had sold at last month’s peak then you’d have $630,000 including dividends. If you had decided to wait three months to make sure it wasn’t another false alarm then you’d have just $450,000.

Bad times are surprisingly good. If you could go back in a time machine and buy stocks at the bottom of every bear market of the past 90 years but had to sell as soon as a recession had officially ended then your annualized return would be a whopping 64%. You would never have lagged the market’s long-run return.

And what if you really can’t sleep at night? Well that’s okay – Covid-19 is enough to worry about! But then you should do one of two things. One would be to dial back the risk you take permanently – no cheating the next time everyone around you is getting rich on pot stocks or whatever the next fad will be. You’ll be that much older and closer to retirement then anyway. The other would be to entrust your money to someone else like a reputable fee-only adviser or a robo-advisor like Betterment or Wealthfront and just check it as infrequently as possible.

Why should you (sort of) like bear markets? Because they’re the time when your attitude can make you a superior investor. Everyone is a genius in a bull market, but tough times are when your mettle matters – no finance degree or superior IQ required. When those glossy brochures from a brokerage firm tell you that the long run return of stocks is 9.6% or whatever, those returns include bear markets that have seen portfolios cut in half or worse.

That’s my usual spiel, which you can read about at length in my book as well, but it’s when I finish giving it and emphasize that nobody on Wall Street knows anything that someone inevitably asks what I think about the market anyway.

I used to get paid a lot to tell people which stocks to buy. Now I get paid a more modest sum to write and edit articles about the same thing. It doesn’t mean you should listen to me about what or when to buy. But, for whatever you may think it’s worth, I’m pretty pessimistic at the moment. If I hold to form then I’ll still be pessimistic when the turning point is reached and we all should be buying stock funds like crazy.

I hear that toilet paper in Hong Kong is worth its weight in gold. Well it isn’t – I checked.

You hear it all the time when people talk about a luxury good or one temporarily in short supply: “It’s worth its weight in gold!”

Very few literally make the grade, though—particularly something an ordinary person might legally buy or consume. Rhodium and heroin don’t count. The latest product to attract the inaccurate label is humble toilet paper courtesy of the coronavirus epidemic, or rather the public reaction to it. A rumor in Hong Kong that supplies would be disrupted set off panic buying and shelves are empty. Supermarket chain Wellcome has instituted a purchase quota.

When shortages emerge bad guys soon sense an opportunity, and it was no different in the relatively crime-free city. Thieves stole 600 rolls with a retail value of $218.

Crime usually doesn’t pay, and it didn’t in this case, either. The thieves were apprehended. Had the rolls been literally worth their weight in gold, at least the effort may have been worth the risk. A typical 227-gram two-ply roll would have to be fenced for $11,895, though.

At that price, even a premium newspaper like this one would present an irresistible arbitrage opportunity for a bathroom-goer—and you could even read it first.