One of the more overused clichés is “it’s like turning around a supertanker.” As a landlubber, I’ll go ahead and assume that’s true in the literal sense. Financially-speaking, though, the business of hauling oil across the world certainly turned on a dime in the past year. Daily earnings collapsed by 99% from last March to the past week as carriers capable of holding two million barrels became very expensive floating storage tanks when there was a glut and are suddenly hunting for cargoes as big exporters try to buoy prices.

Jinjoo Lee and I wrote about the dramatic turn. Our takeaway was that things are looking up for this extremely cyclical business.

A year after their incredible good fortune, an equal basket of four energy shipping firms has lagged the S&P 500 by 70 percentage points over the past year and is right back to its long-term average ratio of price to book value. With life and energy demand returning to normal, this is no time for investors to walk the plank.

It sounds a bit flippant at a time when so many people are seeing their nest eggs melt down on paper, but the message is important. Retail investors lag the market significantly because of timing errors and the biggest mistakes are made at junctures like these. If the 20% bounce from the coronavirus-fueled low turns out to be a dead cat bounce then it will stoke further pessimism and cause people to either sell or to have less of their wealth in risky assets such as stocks once the eventual turn comes.

I’d love to tell you when that turn will be, but I can’t and neither can anyone else. The important thing to remember, though, is that if you were comfortable having, say, 70% of your nest egg in stocks when the Dow was knocking on the door of 30,000 then you should feel the same way at 20,000 or (gulp) 15,000. The richest gains of the next bull market (no, I don’t think this recent bounce was the start of one) probably will come early on. They always have before.

For example, if you put $100,000 into a plain vanilla U.S. index fund at the very start of the last bull market in March 2009 and had sold at last month’s peak then you’d have $630,000 including dividends. If you had decided to wait three months to make sure it wasn’t another false alarm then you’d have just $450,000.

Bad times are surprisingly good. If you could go back in a time machine and buy stocks at the bottom of every bear market of the past 90 years but had to sell as soon as a recession had officially ended then your annualized return would be a whopping 64%. You would never have lagged the market’s long-run return.

And what if you really can’t sleep at night? Well that’s okay – Covid-19 is enough to worry about! But then you should do one of two things. One would be to dial back the risk you take permanently – no cheating the next time everyone around you is getting rich on pot stocks or whatever the next fad will be. You’ll be that much older and closer to retirement then anyway. The other would be to entrust your money to someone else like a reputable fee-only adviser or a robo-advisor like Betterment or Wealthfront and just check it as infrequently as possible.

Why should you (sort of) like bear markets? Because they’re the time when your attitude can make you a superior investor. Everyone is a genius in a bull market, but tough times are when your mettle matters – no finance degree or superior IQ required. When those glossy brochures from a brokerage firm tell you that the long run return of stocks is 9.6% or whatever, those returns include bear markets that have seen portfolios cut in half or worse.

That’s my usual spiel, which you can read about at length in my book as well, but it’s when I finish giving it and emphasize that nobody on Wall Street knows anything that someone inevitably asks what I think about the market anyway.

I used to get paid a lot to tell people which stocks to buy. Now I get paid a more modest sum to write and edit articles about the same thing. It doesn’t mean you should listen to me about what or when to buy. But, for whatever you may think it’s worth, I’m pretty pessimistic at the moment. If I hold to form then I’ll still be pessimistic when the turning point is reached and we all should be buying stock funds like crazy.

The column I edit, Heard on the Street, has to find one mildly ridiculous business story for each issue of the paper, in addition to all the serious, analytical stuff. This usually isn’t a challenge, though there are occasional droughts when we have to dig deep.

Thank goodness for people like Patrick Byrne, CEO of Overstock.com. He is a gift to seekers of corporate hilarity and I was a bit mean to him today.

Patrick Byrne felt a great disturbance among his shareholders, as if millions of voices suddenly cried out for an explanation. This compelled the chief executive officer of Overstock.com to write one of the more bizarre news releases in recent memory about his reasons for selling 900,000 “founder’s shares” of the retailer. “Frankly, I had no idea that shareholders would demand explanations of why and how I might want to use my cash derived from my labor and my property to pursue my ends in life,” he wrote. Mr. Byrne detailed a number of personal projects, including charitable causes, for which he needed the cash. Even after all these years, he is most famous for a different rant about an alleged conspiracy to damage Overstock’s share price involving a “Sith Lord.” Mr. Byrne backed efforts to expose and punish allegedly manipulative short sellers.

Despite some spikes in the share price, the short sellers were basically right. Since the 2005 “Sith Lord” speech, the stock has dropped by 77% compared with a 133% gain for the S&P 500. Perhaps Mr. Byrne should have directed more energy to running the company. Do or do not. There is no try.

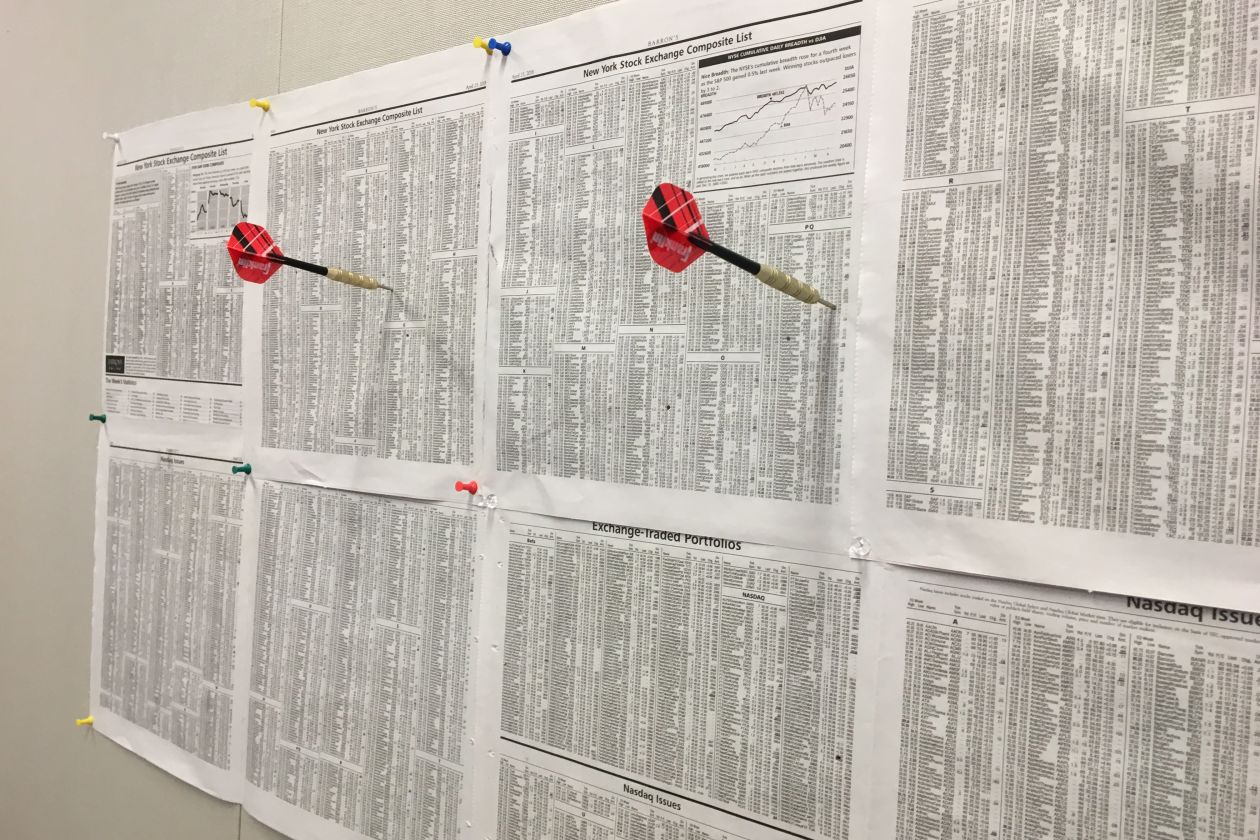

So we decided a year ago to poke some fun at the masters of the universe who unveil their stock picks each year at the Sohn Investment Conference . My team and I decided to throw darts at stock listings and see how things panned out. It was a blowout.

No animals were harmed in this financial experiment, but some human egos were bruised. Burton Malkiel famously wrote in “A Random Walk Down Wall Street” that “a blindfolded monkey throwing darts at a newspaper’s financial pages could select a portfolio that would do just as well as one carefully selected by the experts.” A year ago the journalists at Heard on the Street decided to see if they could beat the crème de la crème—fund managers presenting their stock picks at the annual Sohn Conference in New York. The results were brutal. Heard columnists, not monkeys, threw the darts at newspaper stock listings, but Mr. Malkiel would still approve. The columnists’ eight long and two short picks beat the pros’ selections by a stinging 27 percentage points in the year through April 22. Only 3 of 12 of the Sohn picks even outperformed the S&P 500.

The following memo went out today at The Wall Street Journal from finance editor Charles Forelle.

I’m delighted to announce that Spencer Jakab is the new editor of Heard on the Street. Spencer is a rock of the Journal’s financial commentary. He has been deputy editor of Heard since 2015, and he wrote the Ahead of the Tape column for years before that. His knowledge of companies, markets and financial instruments is encyclopedic. (By my Factiva count, Spencer did nearly 800 Tapes in about 45 months; good luck finding a topic in our universe he hasn’t touched.) He is an incisive financial thinker who embodies the Heard’s spirit of smart, provocative and timely analysis. He also writes killer ledes. He’s the ideal leader for our expansion of the Heard. Before the Journal, Spencer worked at the Financial Times and here at Dow Jones Newswires, and was a stock analyst at Credit Suisse. He is the author of “Heads I Win, Tails I Win,” which is, naturally, a book about investing. Spencer’s move means we are looking for a new Heard deputy. Please get in touch with him if you are interested. And please join me in warmly congratulating Spencer. I believe he’llbecelebratingatOlive Garden. -Charles